Die besten Multibanking-Apps: Alle Konten immer im Blick!

Die besten Banking-Apps kann man nur schwer küren, denn immerhin hängt die Wahl der Anwendung natürlich auch davon ab, welche Eure Hausbank ist. Doch es gibt auch verschiedene Apps, um mehrere Bankkonten oder sogar Kundenkarten und Versicherungen zu verwalten. Wir zeigen Euch, welche.

Sparkasse, Volksbank, Deutsche Bank und andere Banken bieten ihre dedizierten Online-Banking-Apps an. Doch was, wenn man mehr als nur ein einziges Bankkonto verwenden will? Wie wäre es, wenn man PayPal, das Girokonto und die IKEA-Family-Karte mit derselben App verwalten könnte? Dann kommen diese Apps ins Spiel

Outbank 360° Banking

Die Outbanking-App funktioniert mit den Konten von rund 4.000 Banken in Deutschland, Österreich und der Schweiz. Sie erlaubt darüber hinaus die Verwaltung von Girokonten, Kreditkarten, Tagesgeldkonten, Wertpapierdepots und digitalen Services wie Paypal und Bitcoins.

Die App kommuniziert bei der Kontoverwaltung nicht mit den Outbank-Servern, sondern lediglich zwischen Eurem Smartphone und der Bank. Dieses Zero-Knowledge-Prinzip wird konsequent angewendet und erhöht die Sicherheit. Seitdem das Start-up vom Vergleichsportal Verivox übernommen wurde, gibt es hier auch eine Wechselfunktion für Stromverträge.

${app-com.stoegerit.outbank.android}Finanzblick

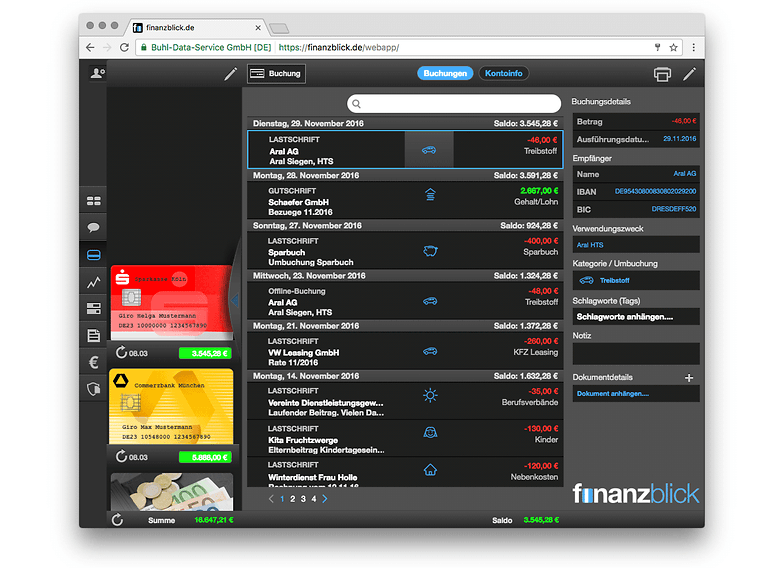

Finanzblick aus dem Hause Buhl erlaubt es, mehrere Giro-, Tagesgeld- und Kreditkartenkonten sowie Eure Versicherungen und Depots im Blick zu behalten. Sogar die Punktestände Eurer Kundenkarten könnt Ihr hier einsehen. Ihr könnt Eure Ausgaben kategorisieren und Budgets festlegen, damit Ihr informiert werdet, wenn diese überschritten wurden.

Da Buhl unter anderem für seine Steuer-Programme bekannt ist, könnt Ihr hier sogar Buchungen auf Relevanz für Eure Steuererklärung prüfen lassen und mit einem Klick in selbige übernehmen lassen. Noch einfacher geht das, wenn Ihr mit dem Scan-Tool Eure Rechnungen digitalisiert. Finanzblick unterstützt Konten und Kreditkarten von mehr als 4.000 Banken in Deutschland. Welche das sind, könnt Ihr hier überprüfen.

${app-de.buhl.finanzblick}Numbrs - Mobile Banking App

Numbrs ist eine Multibanking-App, die Euch nicht nur verschiedene Bankkonten verwalten lässt, sondern auch Kundenkarten integriert. Habt Ihr zum Beispiel eine Bahn Card oder Kundenkarten bei Douglas oder IKEA, könnt Ihr die in der App hinterlegen und habt sie so, wie das Smartphone, immer griffbereit. Überblick über Einnahmen und Ausgaben gibt Euch die integrierte Finanzanalyse.

Numbrs ist vom deutschen TÜV für Datenschutz und Sicherheit zertifiziert und hat Sicherheits-Auszeichnungen von unabhängigen Prüfstellen erhalten. Entsprechend sind alle Informationen hier pseudonymisiert und verschlüsselt.

${app-com.centralway.numbrs}StarMoney

Die Multibanking-App wurde von der Star Finanz GmbH entwickelt, von denen auch die Banking-Apps der Sparkasse stammen. Über die App könnt Ihr Konten und Kreditkarten von über 2.000 Finanzinstituten verwalten sowie Paypal, Aktiendepots, Handyverträge, Ratenkredite und Versicherungen überblicken.

Damit unterstützt die App aktuell weniger Institute als die Konkurrenz, begründet das aber mit dem hohen Sicherheitsstandard, den nicht alle Banken erfüllen. Auf Sicherheit wird beispielsweise auch beim Festlegen des Passworts geachtet, das ganz bestimmte Bedingungen erfüllen muss. Die Starmoney-App gibt es auch als spezielle Version für Tablets.

${app-com.starfinanz.smob.android.starmoney}${app-com.starfinanz.mobile.android.tablet.starmoney}123Banking - Finanzen im Blick

Auch 123Banking bietet mehr Funktionen als das reine Verwalten mehrere Bankkonten. Vom Girokonto, über Kreditkarte, Tagesgeldkonto, Bausparvertrag und das Sparbuch, bis hin zum Paypal-Konto, habt Ihr Eure Finanzen im Blick.

Allerdings gibt es eine Einschränkung: Die Multibanking-App funktioniert nur mit Online-Konten, die den sogenannten HBCI- / FinTS-Standard unterstützen. Die 123Banking-Ap ist laut TÜV- und PCI-DSS-Zertifizierung gut geschützt

Was sind Eure Erfahrungen mit Banking-Apps? Würdet Ihr eine Drittanbieter-App für Euer Konto verwenden oder vertraut Ihr nur der App Eurer Hausbank - wenn überhaupt?

Mhhh... Habe auch mehrere Banken, aber dann auch lieber 2-3 verschiedene Apps!

Anderen Firmen einfach alle Online-Schlüssel in deren App eintragen 😳😵

Wer weiß wohin die Drittapps telefonieren???

Es fehlt Banking 4a von Subsemly, das ist mein persönlicher Testsieger...

Die App heißt aber seit einiger Zeit schon Banking4 ;-)

Verdammt, das sehe ich jetzt zum ersten mal. Jedenfalls auch mein Favorit.

Hey Odo, die gucken wir uns Mal an. Danke für den Tip.

Grabt Ihr eigentlich gerade alle alten Artikel wieder aus?

Hey Thorsten, da sich bei uns ja so einiges ändert, mehr Themenvielfalt etc. Packen wir auch das App-Thema wieder verstärkt an und bringen alte Artikel wieder auf den aktuellen Stand.

Ich nutze Finanzblick auf dem iPad. Allerdings nicht um darin meine Überweisungen zu tätigen, sondern um eine saubere Übersicht und Verlaufsstatistik über die verschiedenen Kontostände zu haben.

Find ich sehr nützlich um einen schnellen Überblick zu bekommen und eine grobe Tendenz erkennen zu können (ob der Gesamtsaldo aktuell eher zu- oder abnimmt).

Kann man zwar auch mit 'ner einfachen Tabellenkalkulation machen, bedarf dann aber einiger Disziplin und Aufwand.

Also ich weis nicht, für so eine multibanking-App gehört schon extrem viel Vertrauen in die App, dass meine Daten Sicher bleiben. Mir persönlich ist das zu riskant. Ich weis es ist nicht ganz so bequem, aber ich nutzte lieber direkt die Apps der einzelnen Banken. Ich denke das ist sicherer, da da nur Ich, meine Bank und deren IT-Diensleister beteiligt sind und nicht noch der Entwickler der App, von dem ich nicht weis wie Sicher er arbeitet.

Sicher, das weis ich auch nicht bei dem IT-Dienstleister meiner Bank, aber dort gibt es doch definitiv mehr gesetzliche Regelungen wie dieser für Sicherheit zu sorgen hat als bei dem Entwickler einer solchen App.

Finanzguru

Schauen wir uns für die nächste Aktualisierung Mal an. Danke für den Tipp.

Hallo,

Ich habe die Beta installiert, aber die App aktualisiert die Konten nicht. Auch habe ich nichts gefunden, um die Aktualisierung händisch anzustoßen....

Nachdem einmal ein Update kam, tut sich nichts mehr...

So nicht gebrauchen.

Rüdiger

Es gibt da auch die App "Finanzblick" Die wirbt auch mit über 4000 Banken... Gibt es dazu Erfahrungswerte? Ich muss sagen, der Gedanke, alle Konten aus einer App zu verwalten, hat schon was.... Momentan nutze ich fünf Verschiedene... Ob die Apps von den Banken sicherer sind als die von Dritten intern, vermag ich nicht zu beurteilen....

Wieso hat man fünf verschiedene Konten? Berufsbedingt?

Hallo, ich glaube, eine Antwort auf diese Frage bringt uns nicht unbedingt weiter..

😉😉😉😉

Weil jede Bank nur 100.000 € absichert

Bin in der beta. Sieht ganz schick aus.

Wie kann man nur Kunde der Sparkasse sein, lernt ihr nicht dazu...

Ich benutze seid Jahren Starmonay...(Vom selben Programmierer wie der Sparkassen-App) Bin bis jetzt zufrieden... Aber wie sagt man so schön... Konkurrenz belebt das Geschäft.

klar die wissen nicht welche Banken ihre Kunden nutzen und entwickeln ins blaue rein ... JD ne ist klar und das ganze vielleicht auch noch kostenfrei ... wo muss ich meine pins einschicken? gehen die dann auch für mich arbeiten?